How do I report an Opportunity Zone fund on my taxes with IRS Form 8997?

Reporting your Qualified Opportunity Fund (QOF) investments accurately is crucial to securing the Opportunity Zone tax benefits they offer. According to the official Instructions for IRS Form 8997, taxpayers must provide a detailed account of any QOF investments they hold at the start of the year, acquire during the year, or dispose of during the year. This ensures that you not only claim the correct deferral or exclusion of gains but also maintain compliance with the Opportunity Zone (OZ) program’s reporting rules.

Below is a comprehensive guide incorporating key points from the official Form 8997 instructions, along with how Form 8949 or Form 4797 factors into the overall filing process.

Determine Your Relevant Forms

Form 8949 or Form 4797

- Form 8949, Sales and Other Dispositions of Capital Assets: Use this form when deferring gain from the sale of capital assets (such as stocks or personal-use property) that you’re reinvesting in a QOF.

- Form 4797, Sales of Business Property: If the gain you’re deferring originated from business or Section 1231 property (such as commercial real estate used in a trade or business), file Form 4797 instead of Form 8949.

You’ll attach the applicable form (8949 or 4797) to your tax return to reflect the deferred gain and confirm that you have reinvested it into a QOF.

IRS Form 8997: Initial and Annual Statement of QOF Investments

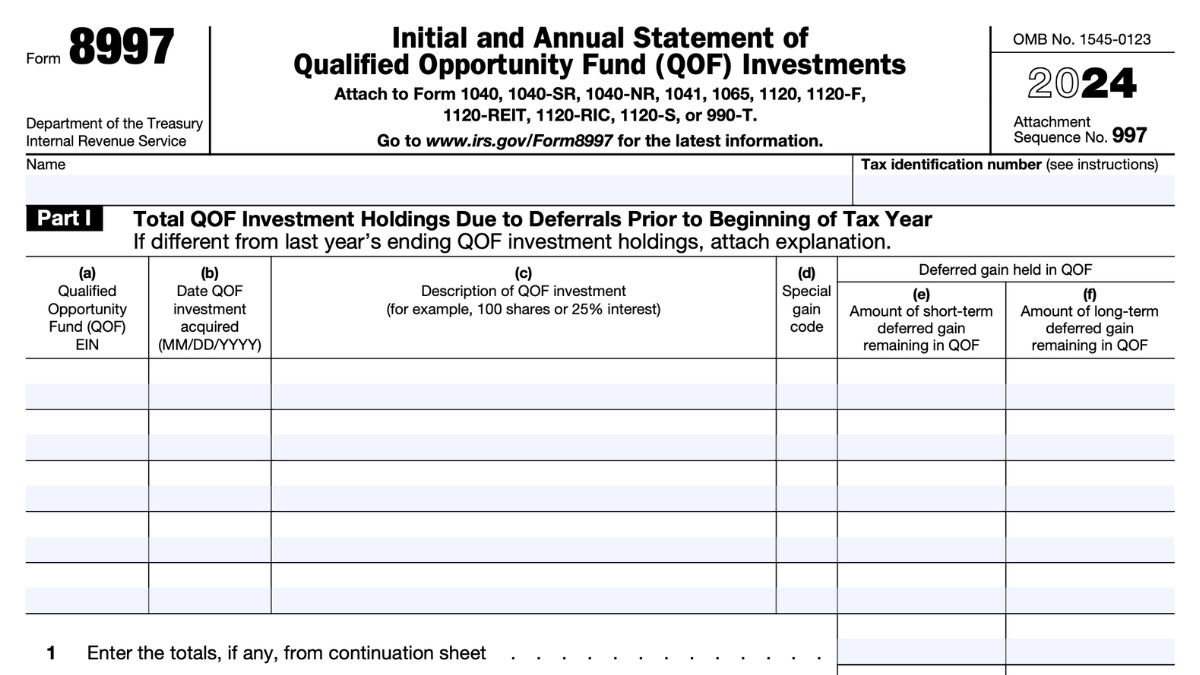

All individuals (and certain pass-through entities, in some cases) must file IRS Form 8997 to detail their QOF investments each year. Form 8997 tracks the life cycle of your QOF investments in four parts:

- Part I – QOF Investments Held at the Beginning of the Tax Year: List each QOF interest you held on January 1, along with the amount of deferred gain still tied to it.

- Part II – QOF Investments Acquired During the Tax Year: Report each new QOF investment acquired during the year, including the date and the amount of deferred gain contributed.

- Part III – QOF Investments Disposed of During the Tax Year: If you sold or otherwise disposed of any QOF interest during the year, record it here. This part helps the IRS determine if you triggered recognition of any deferred gain.

- Part IV – QOF Investments Held at the End of the Tax Year: Summarize all QOF investments you continue to hold on December 31. The amounts shown in Part IV typically carry over to Part I of the following year’s Form 8997, so consistency is key.

Attach Form 8997 to your individual tax return (e.g., Form 1040) or entity-level return if you’re filing through a partnership, S corporation, or C corporation.

Understand the Timeline and Key Steps

- Deferral of Gains: Within 180 days of realizing a capital gain, invest it into a QOF. On your current-year tax return, you’ll use Form 8949 or Form 4797 (as applicable) to note the deferred gain and Form 8997 to identify the new QOF investment.

- Annual Updates: Continue filing Form 8997 each year you hold the QOF investment. This includes carrying over investments from previous years (Part I), listing new acquisitions (Part II), and noting any dispositions (Part III).

- Recognition of Deferred Gain: Your deferred gain becomes taxable on the earlier of the date you dispose of the QOF investment or December 31, 2026. When that happens, report it on Form 8949 or Form 4797 in the year the gain is triggered.

- Potential Tax-Free Appreciation: If you keep your investment in the QOF for at least 10 years, you may elect to exclude any post-investment appreciation from taxable income when you eventually sell or dispose of the QOF interest.

Tips for Compliance

- Accurate Record-Keeping: The instructions for IRS Form 8997 stress the importance of consistency and completeness. Maintain thorough documentation of each QOF investment, including:

- Dates of acquisition and disposal

- Amount of deferred gain contributed to the QOF

- Annual statements or other records from the QOF manager

- Tracking Multiple QOFs: If you have several QOF investments, ensure each is listed separately. Each Part of Form 8997 has multiple rows, allowing you to distinguish gains and holding periods for each fund.

- Aligning Forms 8997 and 8949/4797: The deferral amounts reported on Form 8949 or Form 4797 should match the amounts you list in the appropriate parts of Form 8997. Any discrepancy can raise IRS inquiries.

- Annual vs. Final Return: Each year, Form 8997 provides a “snapshot” of your QOF holdings. When you sell a QOF interest, that disposition is captured in Part III, potentially triggering the previously deferred gain. Keep in mind that even after you recognize the deferred gain, you must still file Form 8997 if you have other QOF investments in place.

Conclusion

Filing your Opportunity Zone investments correctly requires careful alignment of Forms 8949 or 4797 (to document the original deferred gain) and Form 8997 (to report your ongoing QOF activities). By following IRS guidelines—especially the detailed instructions in the IRS Form 8997 publication—you can preserve your tax benefits and remain compliant. When in doubt, consult a tax professional with OZ experience to make sure you’re on track, and always keep meticulous records to document each step of your QOF journey.