Now Available: The Opportunity Zones Playbook

Opportunity Zones Explained: The Beginner’s Guide To OZs

Published January 2026. Written by Jimmy Atkinson, Founder of OpportunityZones.com

What’s new? This new edition of Opportunity Zones Explained includes information on OZ 2.0, rural Opportunity Zones, and how to invest in 2026, 2027, and beyond.

Free Download – Get the PDF Version

Get a PDF version of this guide, Opportunity Zones Explained.

About This Guide

This guide is a practical starting point for understanding Opportunity Zones. It explains the basics of the OZ tax incentive clearly and concisely, without turning into a technical manual.

Written for 2026 — a transition year between the original Opportunity Zones program (OZ 1.0) and the permanent framework often referred to as OZ 2.0 — this guide is designed to help you understand how the incentive works, why timing matters, and whether Opportunity Zones are relevant to you.

If you decide Opportunity Zones are worth exploring further, the final section points you to practical next steps you can take to learn more, including The Opportunity Zones Podcast, our OZ Pitch Day event series and our OZ Insiders Mastermind Community.

Table of Contents

- Background On Opportunity Zones

- What Are Opportunity Zones?

- The Opportunity Zone Map

- Opportunity Zone Tax Benefits

- How Opportunity Zones Work In 2026 (OZ 1.0)

- What Changes With Opportunity Zones 2.0 (And What Doesn’t)

- When A Gain Qualifies For OZ 1.0 vs. OZ 2.0 Treatment

- The Types Of Investments That Qualify (At A High Level)

- Who Opportunity Zone Investments Are For

- How To Learn More About Opportunity Zones

- Additional Mini Guides

- OZ 2.0 Video Crash Course

Free Download – Get the PDF Version

Get a PDF version of this guide, Opportunity Zones Explained.

Background On Opportunity Zones

Opportunity Zones Are More Than Just A Tax Break

Opportunity Zones are often described as a tax incentive. That description is technically correct, but it understates what they really are.

At their core, Opportunity Zones represent one of the most ambitious experiments in modern U.S. economic policy: a long-term effort to redirect private capital into parts of the country that have historically been overlooked by traditional investment flows. Rather than relying on government grants or subsidies, the OZ program 一 first enacted by the Tax Cuts & Jobs Act on December 22, 2017 一 uses the tax code itself as the lever, aligning private investor incentives with public economic goals.

The result is a framework that rewards patience, long-term thinking, and commitment to place. Investors who are willing to deploy capital for a decade or more can access tax benefits that are not merely incremental, but transformational.

Since the program’s launch in 2018, Opportunity Zones have attracted hundreds of billions of dollars in private capital, flowing into real estate developments, operating businesses, and infrastructure projects across thousands of communities nationwide.

The Greatest Tax Incentive Ever Created

Opportunity Zones work by converting past gains into future tax-free growth.

Unlike many tax strategies that simply defer a bill into the future, Opportunity Zones offer something far rarer: the ability to permanently exclude federal capital gains tax on the appreciation of a new investment, if certain conditions are met.

This is why Opportunity Zones are often referred to as the greatest tax incentive ever created.

For long-term investors with capital gains, there is no other federal incentive that offers the same combination of tax deferral, liability reduction, and permanent exclusion of future gains.

Even well-known tools like 1031 exchanges are primarily deferral mechanisms. While a 1031 can effectively eliminate capital gains tax if an investor holds until death, Opportunity Zones offer a path to excluding tax on new investment gains within an investor’s lifetime, after a 10-year hold.

A Program Entering Its Second Era

In 2025, Congress fundamentally reshaped the Opportunity Zones program by making it permanent, via the One Big Beautiful Bill (enacted July 4, 2025). What began in 2017 as a time-limited experiment is now entering a second era, often referred to as OZ 2.0.

Permanence changes behavior. It allows investors, developers, and businesses to plan in decades instead of racing against arbitrary sunsets.

That said, timing still matters. The core OZ 2.0 incentive structure does not fully take effect until January 1, 2027. Throughout 2026, investors will continue to operate under the OZ 1.0 framework, even as the market prepares for new zone designations, revised incentives, and a longer runway ahead.

Understanding what applies now versus what applies next is essential. And it is one of the most common sources of confusion for new investors.

Before diving into the mechanics, it’s worth clarifying what Opportunity Zones actually are.

What Are Opportunity Zones?

A Place-Based Investment Incentive

Opportunity Zones are a place-based investment incentive embedded in Section 1400-Z of the U.S. tax code. The program identifies specific geographic areas, known as Qualified Opportunity Zones, and offers tax benefits to investors who deploy long-term capital into businesses or real estate located within those areas.

These zones are not arbitrary. They are census tracts selected based on income and poverty metrics, using data from the U.S. Census Bureau’s American Community Survey. In practical terms, this means Opportunity Zones are neighborhoods, towns, and rural communities that have experienced persistent economic distress and limited access to private investment.

Why Geography Matters

This is where the policy gets interesting.

Capital is not evenly distributed. In the years following the Great Recession, many affluent regions rebounded quickly, while large portions of the country lagged behind. Investment capital flowed to places that already had momentum, leaving other communities stuck in cycles of disinvestment.

(This idea is detailed in a 2015 white paper published by the Economic Innovation Group, a bipartisan public policy organization that first conceptualized Opportunity Zones and continues to advocate for advancement of the program.)

Opportunity Zones were created to interrupt that pattern.

Instead of mandating investment or expanding federal spending, the program invites private investors to participate voluntarily. The offer is straightforward: if you are willing to invest long-term capital into designated areas, the tax code will reward you.

Designed for Patience, Not Speculation

This is the feature that changes the math.

Opportunity Zones are deliberately structured to discourage short-term speculation and quick flips. To unlock the most powerful tax benefits, an investor must hold their Opportunity Zone investment for at least 10 years.

That requirement aligns the investor’s time horizon with the pace of long-term economic development, which does not happen overnight. As a result, Opportunity Zones tend to attract projects that create durable assets: housing, operating businesses, infrastructure, and long-term job creation.

Flexibility Across Investment Types

Opportunity Zones are also unusually flexible.

The program does not prescribe which industries qualify or what type of project must be built. As long as the investment meets the statutory requirements and is located within a Qualified Opportunity Zone, a wide range of strategies can qualify.

This is why Opportunity Zone capital has flowed not only into real estate, but also into operating businesses across manufacturing, energy, healthcare, technology, and other sectors.

Opportunity Zones are not just about geography. They are about aligning capital with place, time, and intent.

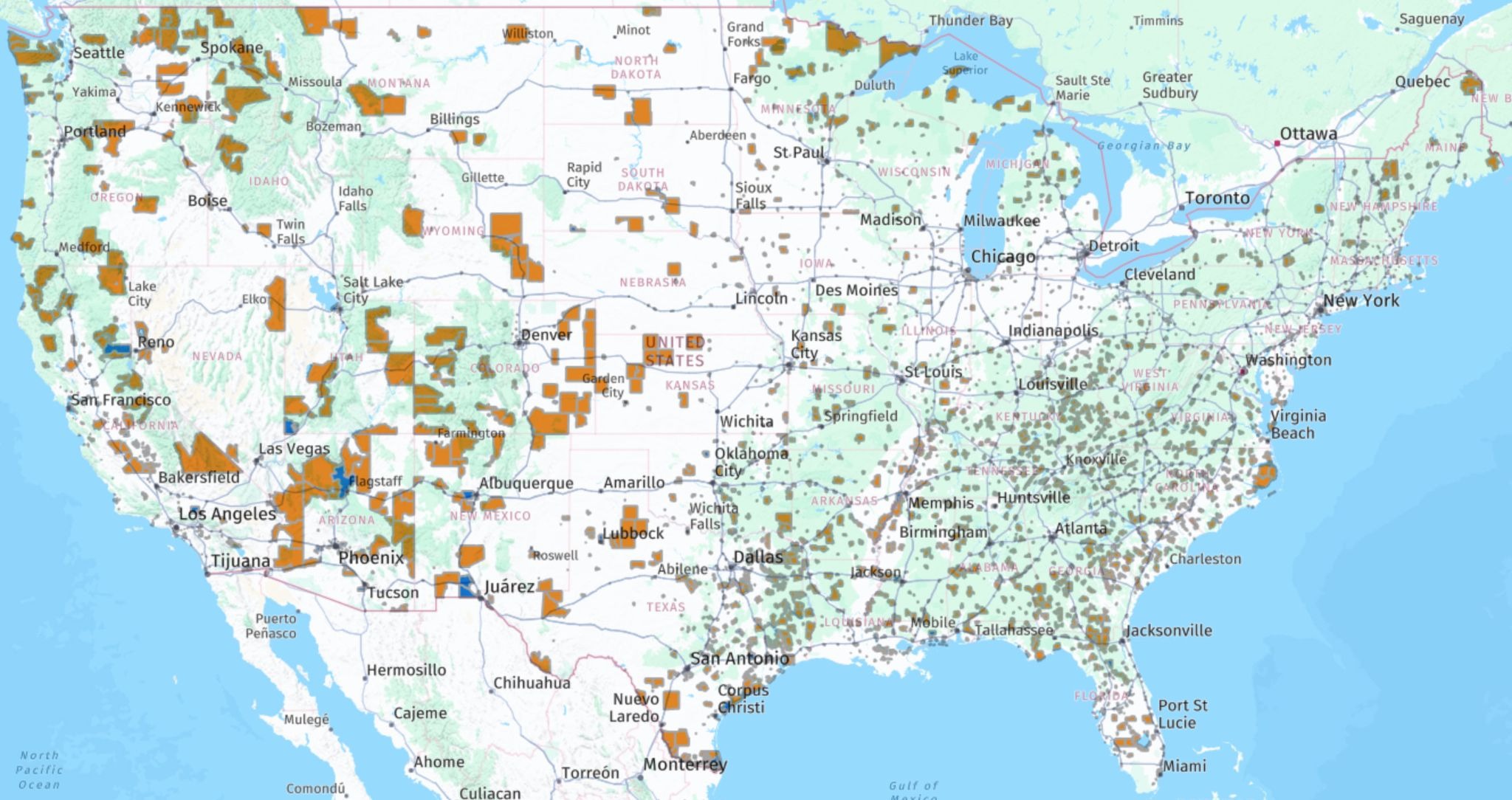

The Opportunity Zone Map

In 2018, the U.S. Treasury and IRS finalized certification of the Opportunity Zones. In total, 8,764 census tracts are certified as Qualified Opportunity Zones. These zones are located in all 50 states, the District of Columbia, and all five inhabited overseas territories. Investments in these areas are subject to powerful tax incentives, as detailed later in this guide.

On September 30, 2025, IRS issued Notice 2025-50, defining which Opportunity Zones qualify as “rural.” Effective July 4, 2025, rural OZs qualify for a reduced substantial improvement threshold.

Web-Based Interactive Opportunity Zone Map

Visit https://opportunityzones.com/map/ for an interactive map and Opportunity Zone lookup tool. You can use this web version to zoom in and search by address.

The New OZ 2.0 Map Coming In 2027

With the enactment of the One Big Beautiful Bill Act on July 4, 2025, the Opportunity Zones program was renewed and made permanent. New low-income census tracts will be designated as Qualified Opportunity Zones in Fall 2026.

This new “OZ 2.0” map will take effect on January 1, 2027. Notably, the current OZ 1.0 map (the tracts designated in 2018) will continue to remain in effect until December 31, 2028. Thus, for a 24-month overlapping period beginning in 2027, there will be two sets of Opportunity Zones in effect.

Refer to the OpportunityZones.com Map for the latest updates throughout 2026.

Opportunity Zone Tax Benefits

At a high level, the Opportunity Zones incentive is built around three distinct tax benefits. Each plays a different role, but together they form the engine that makes the program so powerful.

Tax Deferral: Buying Time For Your Capital

This is the benefit most people notice first.

When you sell an appreciated asset — such as stock, real estate, a business, or certain passthrough interests — you incur a capital gains tax liability. Under normal circumstances, that gain must be recognized and taxed in the near term.

Opportunity Zones allow you to defer recognizing that gain by reinvesting it into a Qualified Opportunity Fund, generally within 180 days of realization. Instead of carving out funds to cover an upcoming tax payment, you keep more capital deployed and working inside the investment.

Deferral does not eliminate the tax. It postpones recognition. But that postponement can materially change outcomes by increasing the amount of capital invested and allowing returns to compound on a larger base.

More on deferral later in this guide. But the length of deferral depends on when your investment is made. Investments made prior to the end of 2026 (OZ 1.0 investments) receive a deferral until December 31, 2026. Investments made after 2026 (OZ 2.0 investments) receive a five-year deferral.

Partial Reduction: Shrinking The Original Tax Bill

This benefit matters less than most people expect — but it still matters.

Under certain timing scenarios, investors who hold a qualifying Opportunity Zone investment for at least five years can receive a step-up in basis on the deferred gain. In plain terms, this means a portion of the original gain may never be taxed at all.

More on this benefit later in this guide. But the availability and magnitude of this benefit depend on when the investment is made and whether it ultimately falls under OZ 1.0 or OZ 2.0 rules. It is helpful, but it is not the primary driver of the Opportunity Zones strategy.

Permanent Exclusion: The Crown Jewel

This is where Opportunity Zones become fundamentally different.

If an investor holds their Opportunity Zone investment for at least 10 years, any appreciation is excluded from federal capital gains tax.

For example, if an investor rolls a $1 million gain into an Opportunity Zone investment and that investment grows to $3 million over 10 years, the $2 million of appreciation can be sold 100% free of federal capital gains tax.

Not just deferred. Not just reduced. Completely excluded from tax!

There is no other mainstream federal incentive that offers this outcome for long-term investors.

The Fourth (Hidden) Benefit: No Depreciation Recapture

In many investments, depreciation can reduce taxable income during the holding period, but a portion of that benefit is often recaptured and taxed upon sale.

Properly structured Opportunity Zone investments are different. Depreciation recapture can also be excluded at exit. This advantage existed under OZ 1.0 and continues under OZ 2.0. It is not new, but it remains one of the most underappreciated aspects of the program.

Using Time As The Multiplier

All of these tax benefits point to the same conclusion: time is the multiplier.

The longer capital remains invested, the more powerful the tax outcome becomes. Opportunity Zones are not about speed or short-term optimization. They are about committing capital for the long haul and being rewarded for that commitment in a way the tax code rarely allows.

How Opportunity Zones Work In 2026 (OZ 1.0)

OZ 1.0 Is Still The Operating System In 2026

Despite the attention on Opportunity Zones 2.0, the rules that govern investments made in 2026 are still the original Opportunity Zones framework — often referred to as OZ 1.0.

That means investors deferring gains in 2026 must evaluate opportunities based on the rules as they exist today, not the rules that will apply in the future. The benefits are still meaningful, but they look different than they did earlier in the program.

The easiest way to understand this is with a simple example.

Example: A $1 Million Capital Gain Invested In 2026 (OZ 1.0)

Assume an investor realizes a $1 million capital gain in 2025 or 2026, and reinvests that gain within the 180-day timeframe into a Qualified Opportunity Fund at some point in 2026. For example, let’s assume the investment into the QOF was made on January 31, 2026.

Here’s how the tax treatment works under OZ 1.0:

- Deferral: The $1 million gain can be deferred, but only until December 31, 2026. At this point in the program, that deferral is essentially nominal. The tax is postponed briefly, but not for years as it was earlier in the program. The liability on this gain is still due on April 15, 2027.

- Basis step-up: There is no basis step-up available for new OZ 1.0 investments. The 15% and 10% step-ups that once applied expired after 2019 and 2021, respectively. As a result, the full $1 million gain is ultimately recognized for tax purposes. (Of note: the amount of gain recognized is limited by the fair market value of the OZ investment on the December 31, 2026 deferral date.)

- 10-year exclusion: This is where the incentive still shines. If the investor holds the Opportunity Zone investment for at least 10 years, any appreciation above the original $1 million investment can be excluded from federal capital gains tax upon sale. Using a QOF investment date of January 31, 2026, the investor in this example will achieve his 10-year hold on January 31, 2036.

- Depreciation recapture: If the investment involves depreciable property and is structured properly, depreciation recapture can also be eliminated at exit.

In short, an OZ 1.0 investment made in 2026 offers little in the way of deferral or reduction of the original gain. But it preserves the most powerful benefit of all: tax-free growth on future appreciation.

For many investors, that alone is enough to justify participation.

Why OZ 1.0 Still Matters

This structure explains why Opportunity Zones did not disappear after the early deadlines of 2019 and 2021 passed.

Even without meaningful deferral or basis step-ups, the ability to exclude capital gains on a decade of appreciation — while the investor is still alive — remains extraordinarily rare in the tax code. For long-term projects and operating businesses, that benefit can dominate the return profile.

OZ 1.0 may be nearing its end, but it is far from irrelevant.

What Changes With OZ 2.0 (And What Doesn’t)

OZ 2.0 Resets The Deferral Clock

Opportunity Zones 2.0 preserves the core architecture of the program but restores balance to the incentive structure by reintroducing meaningful deferral and partial reduction of the original gain.

The same $1 million example makes the contrast clear.

Example: A $1 Million Capital Gain Invested After 2026 (OZ 2.0)

Assume an investor realizes a $1 million capital gain in 2026 or later, and is able to reinvest that gain within 180 days into a Qualified Opportunity Fund on or after January 1, 2027, thereby accessing OZ 2.0 treatment.

Here’s how the tax treatment changes:

- Deferral: The $1 million gain is deferred for five years from the date of investment. Instead of immediately recognizing the gain, the investor receives a meaningful deferral window. Let’s assume a gain realized on August 1, 2026, which is subsequently invested in a Qualified Opportunity Fund on January 15, 2027. That’s when the 5-year clock begins to tick. The gain is ultimately recognized on January 15, 2032, with the tax liability on this gain due April 15, 2033.

- Basis step-up: At the five-year mark, the investor receives a 10% basis step-up on the deferred gain. As a result, only $900,000 of the original $1 million gain is ultimately recognized for tax purposes. (For a rural OZ investment, the basis step-up is 30%.)

- 10-year exclusion: Just like OZ 1.0, if the OZ 2.0 investment is held for at least 10 years, all appreciation above the original invested amount is excluded from federal capital gains tax. In our example, the 10-year clock began ticking on January 15, 2027. As long as the investor holds the QOF investment until January 15, 2037 or beyond, the 10-year hold has been achieved, and he can exit tax-free.

- Depreciation recapture: Just like OZ 1.0, depreciation recapture can be eliminated at exit when structured correctly.

What Stays The Same

Despite these changes, the most important elements of Opportunity Zones remain unchanged.

- The investment must still be held for at least 10 years to unlock the full benefit.

- The incentive is still tied to place-based investing in designated zones.

- The tax advantage still rewards patience above all else.

Opportunity Zones 2.0 does not merely replace OZ 1.0. It builds on it.

Why The Opportunity Zone Transition Year Matters

For investors evaluating Opportunity Zones in 2026, this comparison clarifies the decision framework.

Gains dollars invested in Qualified Opportunity Funds in 2026 fall under OZ 1.0 rules and should be underwritten accordingly. Gains dollars invested in Qualified Opportunity Funds in 2027 and beyond will benefit from the restored deferral and basis step-up features of OZ 2.0.

Both paths can make sense. The key is understanding which rules apply, and why.

Opportunity Zones are no longer a fleeting policy experiment. They are a permanent part of the tax landscape, with a clear line between the original program and its next chapter.

When A Gain Qualifies For OZ 1.0 vs. OZ 2.0 Treatment

At this point, a natural question arises: How do you know whether a capital gain will receive OZ 1.0 treatment or OZ 2.0 treatment?

The answer hinges on when the investment into a Qualified Opportunity Fund is made, not simply when the gain occurs. But the timing rules differ depending on how the gain is generated.

Understanding this distinction is especially important for investors realizing gains in 2026.

The General Rule: It’s About The QOF Investment Date

Opportunity Zone treatment is determined by the date capital is invested into a QOF.

- Investments made into QOFs on or before December 31, 2026 fall under OZ 1.0

- Investments made into QOFs on or after January 1, 2027 fall under OZ 2.0

However, investors do not always invest on the same day a gain is realized. The tax code allows a 180-day window to reinvest eligible gains into a QOF. And when that 180-day clock actually starts ticking depends on the type of gain.

This is where the details get nuanced.

Gains Not Reported On A Schedule K-1 (Direct Individual Gains)

For gains realized directly by an individual — such as the sale of stock, real estate, or a business interest not reported on a Schedule K-1 — the 180-day clock generally starts on the date the gain is realized.

This creates a critical cutoff date of July 6, 2026 (as the 180th day beginning on this date is January 1, 2027).

- A non–K-1 gain realized before July 6, 2026 must be invested into a QOF before the end of 2026.

- That investment would therefore receive OZ 1.0 treatment.

By contrast:

- A gain realized on or after July 6, 2026 can be invested into a QOF in 2027.

- That investment would qualify for OZ 2.0 treatment.

In short, for non–K-1 gains, July 6, 2026 is the practical dividing line between OZ 1.0 and OZ 2.0 eligibility.

Gains Reported On A Schedule K-1 (Pass-Through Gains)

The rules are more flexible for gains reported on a Schedule K-1, such as gains from partnerships, LLCs, or S corporations.

With a gain reported on a Schedule K-1, the taxpayer has three options for electing when to start the 180-day reinvestment period.

- Option 1: The 180-day period may begin on the actual date of the transaction that generated the gain, just as it ordinarily would with a non–K-1 gain.

- Option 2: The 180-day period may begin on the last date of the passthrough entity’s tax year in which the gain occurred. This is typically December 31, which would make the due date June 28 of the following year (or June 27 in leap years).

- Option 3: The 180-day period may begin on the due date of the passthrough entity’s tax return. This is typically March 15 of the following year, which would make the due date September 10 of the following year (or September 9 in leap years).

For a 2026 K-1 gain, this usually means the 180-day period can carry well into 2027, even though the gain itself was realized in 2026.

As a result:

- A K-1 gain realized at any point in 2026 may be invested into a QOF in 2027.

- That investment can therefore qualify for OZ 2.0 treatment.

This timing flexibility makes K-1 gains uniquely well-positioned to bridge the 2026-2027 transition from OZ 1.0 to OZ 2.0.

Why This Timing Distinction Matters

These timing rules explain why two investors with identical economic gains in 2026 may end up with very different Opportunity Zone outcomes.

One investor may be locked into OZ 1.0 treatment because their gain occurred too early in the year. Another may qualify for OZ 2.0 simply because their gain was reported through a passthrough entity or occurred later in 2026.

This is not a loophole. It is how the Opportunity Zone statute and regulations are designed to work.

For investors approaching a liquidity event in 2026, understanding these timelines — ideally before the gain is triggered — can materially affect the tax outcome.

The Types Of Investments That Qualify

At this point, many first-time readers assume Opportunity Zones are simply about buying real estate in the right location. That assumption is understandable — and incomplete.

Opportunity Zones are not an asset-class incentive. They are a structure-and-use incentive. What matters is not just what you invest in, but how and where the investment operates.

Qualified Opportunity Funds Are The Gatekeepers

All Opportunity Zone investments must flow through a Qualified Opportunity Fund.

An investor does not elect Opportunity Zone treatment on a tax return in isolation. The tax benefits attach only when capital gains are invested into a compliant fund structure that meets specific requirements.

At a high level, a Qualified Opportunity Fund must deploy the vast majority of its assets into qualifying Opportunity Zone assets. These assets generally fall into one of two categories:

- Qualified Opportunity Zone Property (QOZP), or

- Equity interests in a Qualified Opportunity Zone Business (QOZB) that holds Qualified Opportunity Zone Business Property (QOZBP).

The distinction matters, but the unifying theme is this: Opportunity Zones reward active deployment of capital into qualifying assets.

Real Estate Can Qualify — But Not All Real Estate Does

Real estate is the most popular use of Opportunity Zone capital, but it is not a blanket qualifier.

To qualify, real estate generally must either:

- be newly constructed in an Opportunity Zone; or

- be substantially improved (doubling the value of the structure within a 30-month period).

Simply acquiring raw land or an existing building and holding it does not qualify.

This requirement is intentional. Opportunity Zones are designed to incentivize development, rehabilitation, and economic activity — not land banking or passive appreciation.

Operating Businesses Also Qualify

One of the most underappreciated aspects of Opportunity Zones is that operating businesses can qualify, not just real estate projects.

Manufacturing companies, service businesses, energy projects, healthcare providers, and technology companies have all used Opportunity Zone capital to begin or expand operations within Opportunity Zone locations.

For these businesses, the incentive can be especially powerful. Patient capital combined with long-term tax efficiency can support growth strategies that would otherwise struggle to attract traditional financing.

This is often where the Opportunity Zones story shifts from abstract to tangible.

Why Execution Matters More Than Eligibility

It is one thing for an investment to qualify on paper. It is another for it to succeed economically.

Opportunity Zones do not guarantee returns. And they don’t turn a bad deal into a good one. But they do materially change the tax treatment of profitable deals. Opportunity Zones can turn a good deal into a phenomenal one.

This is why most experienced investors spend far more time evaluating sponsors, business plans, and execution risk than they do chasing technical eligibility alone.

Qualification is the starting line, not the finish line.

Who Opportunity Zone Investments Are For

Opportunity Zones are powerful — but they are not universally appropriate for all investors.

Understanding whether an Opportunity Zone investment may fit into your portfolio is just as important as understanding how it works.

Opportunity Zones May Be A Fit If You:

- Have significant U.S. capital gains tax liabilities.

- Are comfortable committing capital for 10 years or longer.

- Prefer tax efficiency tied to long-term growth.

- Value patience over liquidity.

- Are an accredited investor.

For these investors, Opportunity Zones can meaningfully reshape after-tax outcomes.

Opportunity Zones Are Likely Not A Fit If You:

- Need near-term liquidity.

- Are uncomfortable with multi-year uncertainty.

- Have limited or no capital gains.

- Expect tax incentives to compensate for weak execution.

- Are not an accredited investor.

Opportunity Zones amplify outcomes. They do not rescue bad investments or eliminate risk.

This self-selection is healthy. The incentive was designed for long-term capital, not for everyone.

Why Sophisticated Investors Approach OZs Differently

Experienced Opportunity Zone investors tend to focus less on “maximizing the tax benefit” and more on aligning incentives.

They look for:

- Sponsors with solid track records who can operate over long time horizons.

- Projects where patient capital is genuinely additive.

- Business plans that are profitable without tax benefits.

The tax incentive enhances the result. It does not define it.

That mindset shift often marks the difference between curiosity and serious participation.

How To Learn More About Opportunity Zones

If you’ve made it this far, you now understand Opportunity Zones better than most people encountering them for the first time.

You understand:

- Why the incentive exists.

- How the tax benefits work.

- How OZ 1.0 and OZ 2.0 differ.

- Why timing matters in 2026.

- What qualifies, and what doesn’t.

What comes next depends on how deeply you want to engage.

Path One: Stay Informed

Opportunity Zones are evolving. New zone designations, new guidance, new projects, and new interpretations will continue to shape the landscape — especially as OZ 2.0 fully takes effect.

If your goal is to stay current and deepen your understanding over time, the best place to start is our ongoing educational content:

- The Opportunity Zones Podcast, where we interview fund managers, developers, policymakers, and tax professionals on how OZs work in the real world

- The OpportunityZones.com YouTube channel, where we break down Opportunity Zone concepts, explain new developments, and explore case studies in a more visual, conversational format

Both are designed to help you stay informed as the program enters its permanent phase.

Path Two: Learn By Observation

For many investors, clarity comes not from theory, but from exposure.

Seeing how real Opportunity Zone projects are structured — how sponsors frame their strategies, how different approaches compare side by side, and how capital is actually deployed — often accelerates understanding far more than reading alone.

That’s the purpose of OZ Pitch Day.

OZ Pitch Day is a live (and recorded) event series where Opportunity Zone fund managers and developers present their investment strategies to an audience of investors. It’s designed to be educational first, with no obligation to invest.

If you want to see how Opportunity Zones are being used in practice, this is the fastest way to build context.

Path Three: Go Deeper

At a certain point, most serious investors realize they don’t just need more information. They need better judgment and a sounding board.

That typically comes from ongoing education, curated insight, and conversations with others who are actively navigating Opportunity Zone investing at a high level.

OZ Insiders is our private Mastermind community for investors, fund managers, developers, and advisors who want to gain knowledge, build trusted relationships, and get the edge for OZ 2.0 success.

Members get access to advanced discussions, expert sessions, and a trusted peer network focused on long-term execution — not hype.

It’s not for everyone. But for those committed to understanding Opportunity Zones at a serious level, it’s where the most valuable conversations happen.

Free Download – Get the PDF Version

Get a PDF version of this guide, Opportunity Zones Explained.

Additional Opportunity Zone Mini Guides

Mini Guide: Opportunity Zone Tax Benefits

Updated for OZ 2.0. To encourage investment in economically distressed areas, there are multiple powerful Opportunity Zone tax benefits available to U.S. taxpayers who reinvest eligible gains into Opportunity Zones via a Qualified Opportunity Fund. The ability to achieve unlimited tax-free growth makes Opportunity Zones the greatest tax incentive ever created.

Mini Guide: Two Ways To Invest In OZs

Updated for OZ 2.0. In general, there are two ways to invest in Opportunity Zones: 1) Active QOF Investment: An investor who has realized a gain and wishes to take a hands-on approach to managing his next investment as a general partner, or GP, may create his own Qualified Opportunity Fund; 2) Passive QOF Investment: Alternatively, an investor may take a more “hands off” approach by investing his gains into a third-party Qualified Opportunity Fund that is raising equity from investors.

Mini Guide: How To Start Your Own OZ Fund

Updated for OZ 2.0. Qualified Opportunity Funds (QOFs) were created as part of President Trump’s Tax Cuts & Jobs Act of 2017. These Opportunity Zone funds provide massive tax incentives for re-investing capital gains in some of America’s most economically distressed communities. Starting your own Qualified Opportunity Zone Fund is easy.

Mini Guide: Opportunity Zones vs. 1031 Exchanges

Updated for OZ 2.0. Most sophisticated real estate investors are familiar with Section 1031 exchanges, and related Delaware statutory trusts (DSTs). Opportunity Zones appear similar at first glance. But there are some substantial differences.

Mini Guide: The Best Opportunity Zone Resources To Learn More

Updated for OZ 2.0. Opportunity Zones were nominated at the state level in the first half of 2018 before being certified by the U.S. Department of Treasury. This page features a list of Opportunity Zone resources from OpportunityZones.com, plus additional resources from federal, state, local governments, and national advocacy and economic research organizations.

Mini Guide: A Brief History Of Opportunity Zones

Updated for OZ 2.0. Opportunity Zones are a place-based economic development program that was first conceptualized by the Economic Innovation Group (EIG) in a 2015 white paper, Unlocking Private Capital to Facilitate Economic Growth in Distressed Areas.

Watch Our OZ 2.0 Video Crash Course

Want a video version of this guide? Watch our 50-minute crash course that’s now available on YouTube.

About The Author

Jimmy Atkinson is a leading educator and advocate in the Opportunity Zones ecosystem. He founded OpportunityZones.com in 2018 as a dedicated resource for investors, fund managers, developers, and advisors seeking clear, practical guidance on the Opportunity Zones incentive.

Jimmy is also the founder of OZ Insiders, a private Mastermind community where members can gain knowledge, build trusted relationships, and get the edge for OZ 2.0 success.

Jimmy also hosts The Opportunity Zones Podcast, where he interviews fund managers, developers, policymakers, and industry experts on how Opportunity Zones work in practice.

Since the program’s inception, Jimmy has been closely involved in the evolution of Opportunity Zones, helping thousands of investors better understand the policy, the mechanics, and the real-world execution of OZ investments.